The Top 2015 Indian Real Estate Market Statistics You Shouldn’t Miss

Being the largest employer after agriculture, and with an estimated growth rate of 30% over the next decade, Indian real estate sector is surely one of the most recognized sectors globally. This growth of corporate environment and demand for office space beautifully complements the growth of this sector, be it the top 6 cities, or the tier-II ones.

The real estate sector comprises of two sub-sectors – housing (residential) and commercial.

Residential

This segment contributes more than 80% to the real estate sector.

There are basically three types of housings – Affordable, Mid-income and Luxury housing.

1. Affordable housing: This segment accounts for 85% of total residential demand. Assuming, a 1BHK and 2BHKs require an average of 400 sq. ft. individually, then, India needs to develop 14-16 billion square feet for this segment alone.

2. Mid-income housing: This segment accounts for 7% of the total housing demand. Assuming a 2-3BHK to be consuming an average of 1000 sq. ft., then, 28-32 billion square feet of development is required for this section.

3. Luxury housing: In 2012, India showed second highest growth of 22.2% in its HNI population. India’s HNI population is expected to more than triple by 2018.

Accordingly, there has been new launches of townships.

The absorption rate that has been falling steeply since 2013 is now taking up flight and moving towards complete absorption of the projects and thus, creating an urgent need to plan new townships and apartments.

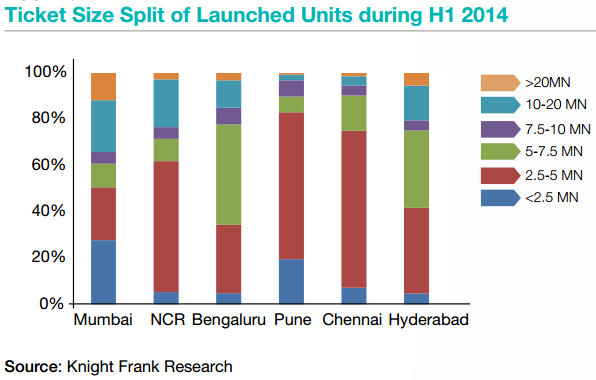

If the ticket sizes are taken into account, Pune appears as the most affordable city, as 83% of the new launches fall below the ticket size of 5 mn and lead to perfect absorption and least number of vacancies.

If we were the determine the healthiest market among the six major cities of India, it would be Bengaluru with a low QTS and age of unused inventory. It comes off as the most balanced market, even though it witnessed a steady drop in sales volume. How?

Developers in Bengaluru remained vigilant to the falling absorption levels, and reacted smartly by deliberately reducing the number of new launches.

In contrast, the health of the Mumbai’s residential market is the poorest, with highest QTS and a huge chunk of unused inventory.

Opportunities:

1. Urbanization: Due to the urbanization of nearby areas around the major six cities like NCR for Delhi, there is a need for 2 million houses each year, largely in the affordable housing segment. This presents a business opportunity of close to 9 trillion INR.

2. Nuclear families: Since 35% of India’s population falls between the age bracket of 15-35 years, the demand for housing will rise to almost 35% in the upcoming 15 years.

Commercial

This segment mainly depends on growth in services and industrial sectors of the economy such as logistics, warehousing, and manufacturing.

1. Office: The two of the major occupiers of office space in India are IT/ITeS and BFSI.

2. Retail: Retail is growing too, at an expected rate of 8% CAGR.

3. Industrial: The Indian government is taking measures to promote this segment.

According to Knight Frank’s research, Mumbai is so far the best city for commercial real estate investment, at an ROI of 12-19% in the upcoming 5 years, closely flowed by Bengaluru and Delhi-NCR.

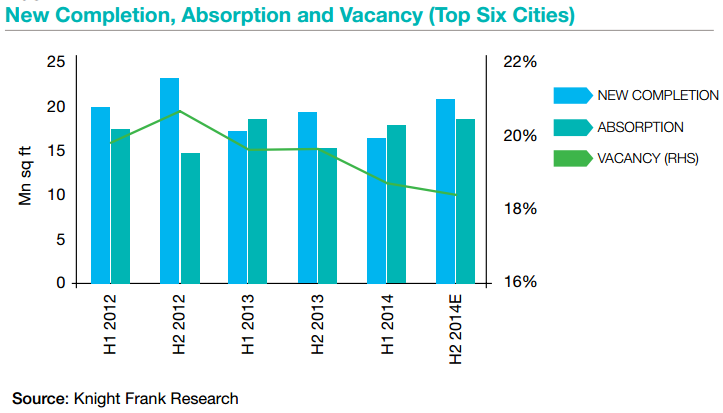

As is visible from the combined data of top 6 Indian cities, the office market have been recovering steadily with vacancy levels falling from 21% to less than 19%. This shows tremendous opportunity for launching new projects as the absorption is slowly catching up too.

If sector-wise absorption is split and considered, then The IT/ITES sector again continues to lead across all the cities, except for Mumbai. In Mumbai, it is the demand from the manufacturing sector that has dominated, flowed by the other services.

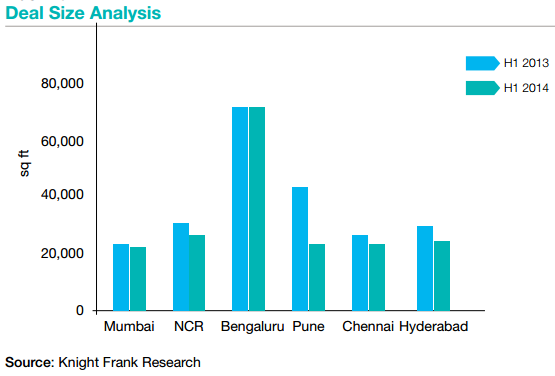

There is a clear sign of improvement in the commercial real estate market, since there is an increase in the number of deals which means a higher participation in transaction by occupiers. Nonetheless, the average deal size hasn’t reduced significantly in most cities. Pune witnessed the steepest plummet while Bengaluru has been able to maintain it, despite a substantial jump in the number of deals.

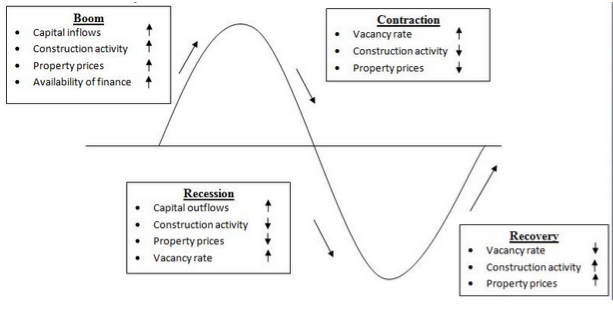

All this can be very well explained if we once understand the real estate cycle.

The Real Estate Cycle:

1. Boom: In this period, capital inflows rise and so does the availability of finance. As a result, there is a respective increase in construction activity and property prices.

2. Contraction: This period observes a rise in the vacancy rate and a drop in property prices. Consequently, construction activities slow down.

3. Recession: This is known as a period of high capital outflows with less ROI, as in there is a drop in property prices so they don’t get used and hence, vacancy rate increases. This leads to further slowdown of construction activities.

4. Recovery: As the name suggests, this period is marked by a drop in vacant number of properties, and a consequent increase in construction activity and property prices.

How To Make The Most Of This Cycle?

Learn the key growth drivers and how a consumer reaches to the buying stage – understand his whole purchase journey.

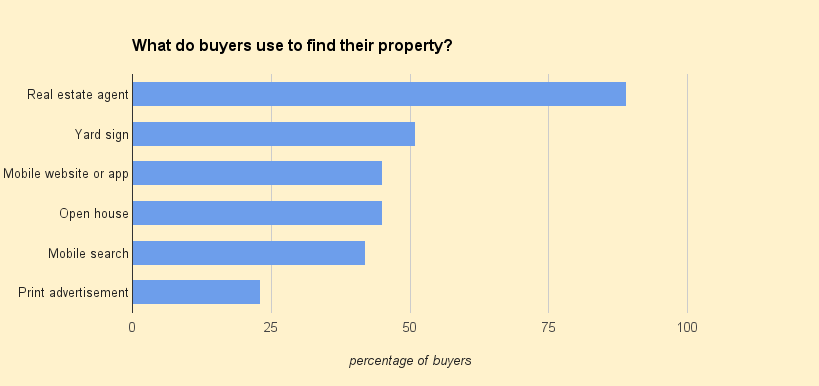

Opportunity #1: Go Mobile

Most customers are reaching property sites via the mobile path. As is evident from the graph above, share of mobile website, app and search is clearly beating print advertisement. If predictions are to be believed, these routes will beat even the real estate agents and yard signs.

Going mobile is the next logical step in the real estate cycle.

Opportunity #2: Declining Interest Rates

A stable Government at the center has infused the nation with optimism. Plus, there are declining interest rates and an extension of exemption limit from 1.5 lakh to 2 lakh on interest on a loan in respect of the self-occupied property. This will ensure a good pick up in the residential units.

Challenge #1: Rising Material Cost

Building materials like cement, steel and bricks along with labor cost make up for almost 75% of the total construction cost and they are expected to increase.

Challenge #2: High Inventory Levels

As is explained from the real estate cycle, there was a negative growth in housing absorption over the past two years hence, there are a lot vacant square feet.

Growth opportunities:

There has been separate funds allocated to develop 100 new smart cities in the 12th Five year plan (2012-17) where Indian government would be investing USD 1 Trillion in the infrastructure.

So for a real estate developer, there are ample reasons to work and launch new projects as the economy and pitical scenario is in favor of this industry.