Understanding the Value Chain in Indian Online Real Estate Services

Real estate is an ever-growing industry, even though it hits certain rough patches, by and large, it continues to boom. In the last couple of years, we saw a number of tech startups enter the space of online real estate services.

Housing.com made big waves in the news with its $90 million investment from Softbank. And soon after, it was 99acres.com which raised $120M from Info Edge. Another major player is Commonfloor which raised INR 64 Cr (roughly $10 Mn) and a $30 Mn in Series E led by its existing investor Tiger Global.

Despite the fierce going on competition in the online real estate services, there are still tremendous opportunities left in the real estate sector. But how much do we understand the value chain of this sector?

This is exactly what we’ll cover today – a look at the individual segments of this value chain:

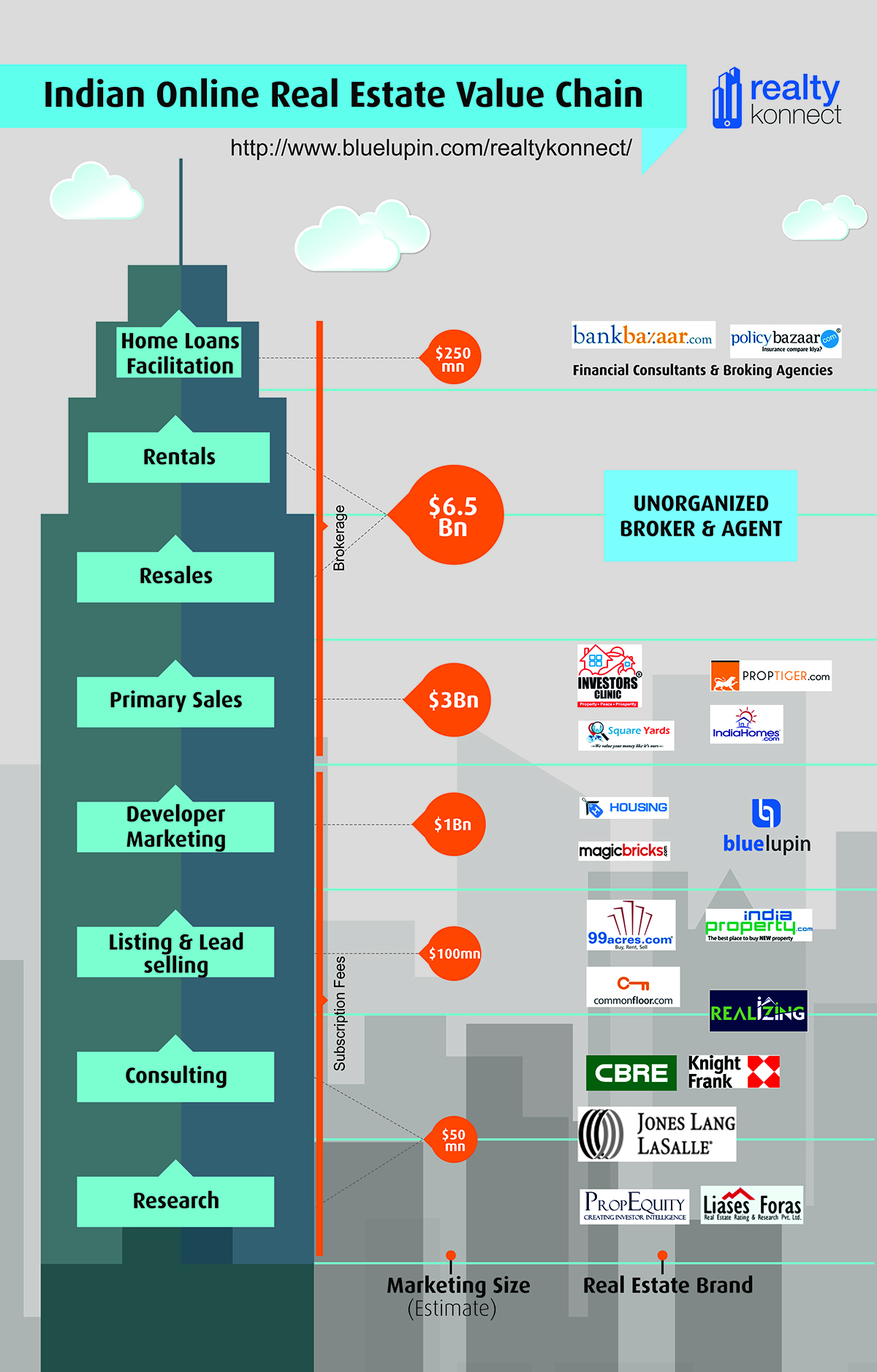

1. Research and consulting:

Dominated mostly by international players like JLL and Knight Frank, this segment accounts for almost $50 million of a net worth of the value chain. Indian players have tried to foray into data science but this research was left reserved largely for B2B companies.

Upcoming Indian players:

www.crisil.com

www.imrbint.com

Not many, hmm?

That’s a window of opportunity for research firms to specialize in real estate researches.

Opportunity: Property transaction is probably the most valuable transaction a person makes in his lifetime and most of them are burdened under EMIs and plunge in their life’s savings. For this, they need research to avert the risks and invest stress-free. There’s a whole new arena of opportunity in this part of the value chain.

2. Listings and lead Selling

With a net worth of $100 million, this segment has quite a lot of Indian players at the moment, such as:

99acres.com

commonfloor.com

indiaproperty.com

There is a war going on over the control of supply. Even general classifieds websites such as OLX and Quickr are also venturing in this segment.

But the truth is that this is basically a broker’s market from the perspective of monetization. If observed carefully, almost 95% of the listings are uploaded by brokers and not the end consumers.

Opportunity: Any means to help these brokers close more sales, and make their day more productive.

3. Developer Marketing:

This is an emerging market worth $ 1 Billion, that everyone is trying to capture due to a significant shift in the marketing budgets when moved from print to online.

Current players in India are:

magicbricks.com

housing.com

MobileKonnect by Bluelupin

What most online players are focusing on is ‘virtual reality’ kind of innovations such as 3D glasses, drone views, virtual walk-throughs, etc. These are definitely helpful but only to an extent. When it comes to closing a transaction using these upcoming technologies, they are overrated.

What needs to be done is smart content telling, not a run-of-the-mill glossy brochure, but something that positions their product as far more superior to their competition.

4. Primary Sales

This segment accounts from more than $3 billion of net industry worth and is highly lucrative and organized. The Segment includes the prime transaction between the buyer and the developer. There is no individual-to-individual resale, only direct sales from developers.

Top players include:

Investor’s clinic

Square Yards

Proptiger

IndiaHomes

Opportunity: There lies a huge opportunity in the realm of aftermarket services such as resale assistance and portfolio management that can become massive differentiators, if tapped by the incumbents.

5. Resale and rentals:

Not B2B, not B2C, this is a C2C market – The biggest market and unsolved puzzle of the real estate story is this segment – resale and rentals. There are absolutely no online players and with a net worth of $6.5 billion, this is a gold mine left untouched. It is still dominated by brokers and agents. Why is the scenario like this?

#1 the inability to control the supply and

#2 the involvement of cash

If in future, some players try to get in to disrupt the scenario, the transactions would become more digitized and regulated.

Opportunity: A self-regulating ‘deal room’ kind of C2C digital marketplace is needed.

6. Home loans facilitation:

This $250 million worth of market comprises of facilities that help compare multiple options and choose the one that best suits the customer.

Major players include:

bankbazaar.com

policybazaar.com

financial consultants and broking agencies

Opportunity: Since a major share is taken up by financial consultants and broking agencies, there lies a lot of opportunity in this market to capture the paying customer’s mindshare.

Closing Thoughts:

This online real estate is a multi-billion value chain with many sub-markets within.

Despite having so many well-funded players, there is no one that could actually captivate the paying customer’s mindshare, let alone get hold of the share of his wallet.

Also, with so many existing players, this is not a ‘winner-takes-all’ market as there wouldn’t be any that would be able to capture the whole market at once. However, there is sufficient room for everyone to coexist and compete.

Beyond just lead generation and transaction, there are bigger battles to be fought and won.

What are your thoughts on the value chain of the real estate industry?